Regulatory uncertainty surrounding stablecoins was a large blocker in their mainstream adoption. If you need a refresher on what a stablecoin is, read more on this article here.

Over the past year, increased clarity surrounding stablecoins and money transfers has made it safe for both institutions and consumers to utilize the technology.

Major banks such as JPMorgan and Bank of America are entering the space, with bold proclamations that all accounts will be on-chain in the next few years. With clear rules now in place, it is only a matter of time until stablecoins and crypto become a major part of our everyday financial lives.

Clear Rules Have Finally Arrived

Before the GENIUS Act, there was no regulatory oversight on stablecoins. Large consumer apps such as Robinhood and Coinbase were actively encouraging the US government to establish fair laws surrounding blockchain technology. This push was part of a broader effort to compete with traditional banks while offering consumers superior financial services.

The GENIUS Act passed in July 2025—and with it came a few clear changes:

Reserve Requirements: Stablecoin issuers must back their tokens on a one-to-one basis with high-quality liquid assets, ensuring every digital dollar is redeemable for a real dollar.

Federal and State Oversight: Issuers must be chartered and supervised at either the federal or state level, bringing stablecoins under the same regulatory umbrella as traditional financial institutions.

Consumer Protection Standards: New requirements ensure transparency in reserves and redemption processes, giving users confidence that their funds are safe and accessible.

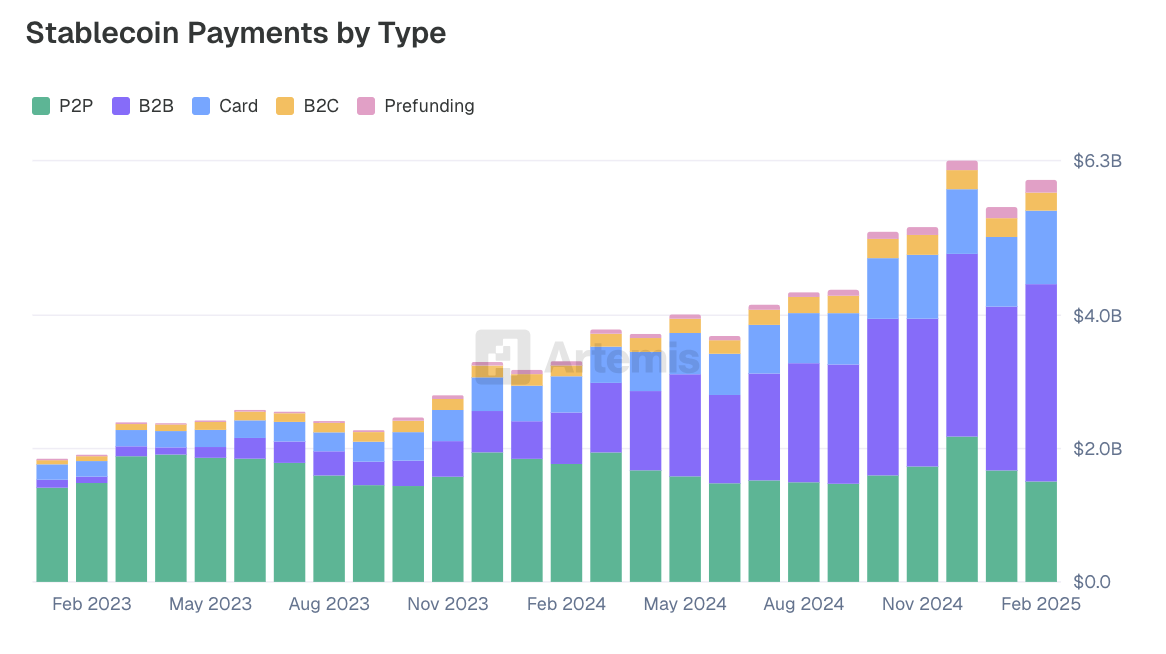

With this regulatory framework in place, the financial industry finally had the clarity it needed to move forward. One in four CFOs expect to integrate cryptocurrencies into their treasury services within the next two years. Let's explore the most recent examples:

Stripe Builds A Blockchain

Stripe processes over a trillion dollars in payments annually, making it one of the largest payment processors in the world. In September 2025, shortly after the GENIUS Act passed, Stripe announced Tempo—a new blockchain built specifically for payments in partnership with Paradigm.

Stripe has announced plans to move their existing infrastructure to Tempo, while also supporting use cases designed for companies that want to build payment systems using stablecoins. Early partners include OpenAI, Kalshi, Shopify, and Revolut.

America's Biggest Banks Team Up

In May 2025, JPMorgan Chase, Citigroup, Wells Fargo, and Bank of America announced they're exploring a joint stablecoin project. The goal is to create a shared network that functions like Zelle but runs on blockchain rails, enabling instant settlement, 24/7 availability, and programmable payment logic that traditional banking infrastructure can't support.

This isn't the first time banks have collaborated in response to new competition. In 1970, Bank of America gave up sole control of its BankAmericard program and turned it into a consortium owned by multiple banks. That consortium became Visa. The distributed ownership model allowed banks to share infrastructure costs and interoperability standards while still competing for customers. This is exactly what they're attempting with stablecoins today.

What Does All This Actually Mean?

E-Commerce Gets an Upgrade

Online merchants can receive stablecoin payments with significantly lower fees than traditional credit card charges. Some platforms are even offering cashback incentives to merchants who accept stablecoins, creating additional financial incentives to drive adoption.

Business Payments Become More Efficient

Companies settling invoices with suppliers can skip the slow, expensive wire transfer process entirely. Stablecoins enable instant settlement 24/7, improving cash flow and reducing transaction costs. This addresses a common problem: cash sitting idle offshore while waiting for correspondent banks to settle payments, particularly over weekends or through slower local payment rails.

Cross-Border Payments Get Faster and Cheaper

Sending money internationally through traditional banks can take days and cost significant fees. Stablecoins can move anywhere in the world in seconds for pennies. For companies operating across multiple jurisdictions, correspondent banking can be complex. Treasury teams manage dozens of banking relationships, currencies, and cut-off times across time zones. This creates three problems:

Higher borrowing costs from trapped cash that cannot be deployed efficiently

Suboptimal hedging based on incomplete or delayed data

Excess bank fees for accounts holding idle liquidity

Some banks solved this problem by offering tokenization services for instant fund movement between entities, but only within their own network. Stablecoins work across banks and function more like cash.

The Future is Stable(coins)

With the GENIUS Act providing a clear rulebook, the era of regulatory uncertainty for stablecoins is over. Financial giants like Stripe and America's largest banks are actively building on blockchain rails. This shift promises faster, cheaper, and more efficient payments for businesses and consumers alike. The debate is no longer about if stablecoins will be adopted, but how quickly they will become the new standard for how we move money and invest on a global scale.